Your retirement journey begins here !

8 Simple steps to being investing in yourself and your future.

Step 1

The first step of anyjourney is the most important. It gives you asense of direction and starts you toward a destination. The same is true of your journey to retirement. By enrolling in your employer’s retirement plan, you are taking an important first step.

Go to www.mykplan.com/enroll Click on the “Get Started” button to begin your enrollment process.

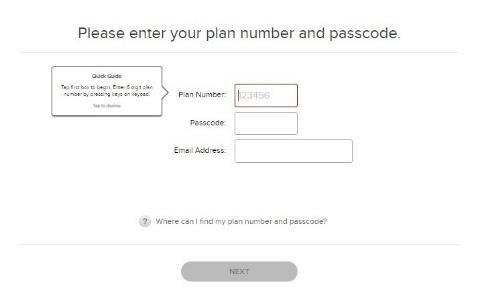

Step 2: Enter your plan number, Passcode and Email address

The plan number and passcode were provided to you during an enrollment meeting. If you have misplaced the information or did not receive it, please contact your planadministrator. You can also call ADP’s Participant Service Team at 800-MyK-Plan (800-695-7526) and a representative will be able to assist you with this information.

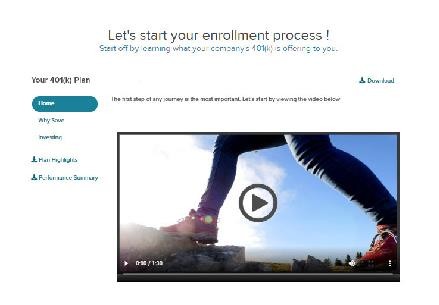

Step 3: Explore and Enroll

Take some time to explore information on the site. Information about your employer’s retirement plan is located in the Plan Highlights and the Performance Summary section provides details about the investments. You can also download a full education kit by clicking the download button. Click on the “Enroll Now” button to move to the next step in your journey.

Step 4: Verify your date of birth

Providing this information allows ADP to provide you with information that may be helpful during the investment election process. None of the information you enter to complete your enrollment will be storedon this site.

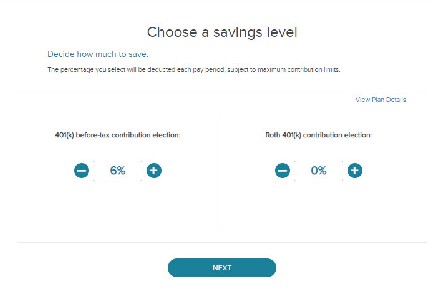

Step 5: Select your contribution type and percentage

Duringthisstep, you will select how you want to contribute to the Plan(before-taxor Roth 401(k) or a combination of both). You can also select the percentage to each contribution type. You can click “View Plan Details” to view your Plan’s highlights, which will contain more complete information on the Plan’s contribution types and contribution percentage limits. Click on “NEXT” to continue to the next step.

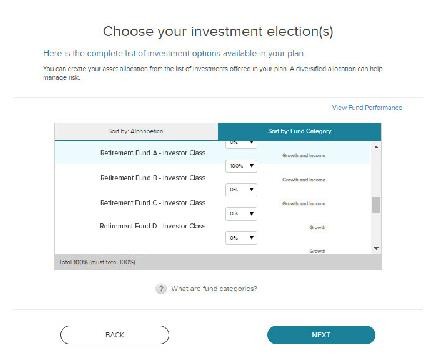

Step 6: Investment selection

During this step, you will select your investments and the percentage you want to contribute to each. You can view investment performance by clicking on “View Fund Performance.”

If your plan includes target date funds and you wish to invest in one of these funds, you may do so. Generally, you would select the fund that is closest to the date you will turn age 65. However, you do not need to select this fund. You can also select a mix of investments to create your own asset allocation. The total of your investment election much equal 100%.

Click on “Next” to continue to the next step.

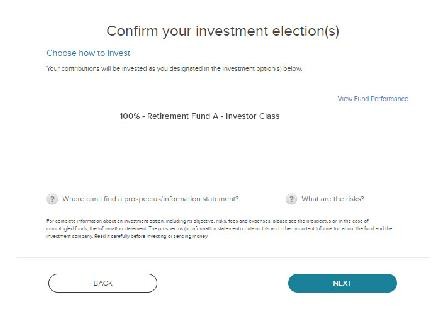

Step 7: Confirm your investment election(s)

Review your investment election(s). If you need to make changes, selectthe “Back” button. If everything looks good, then select “Next.”

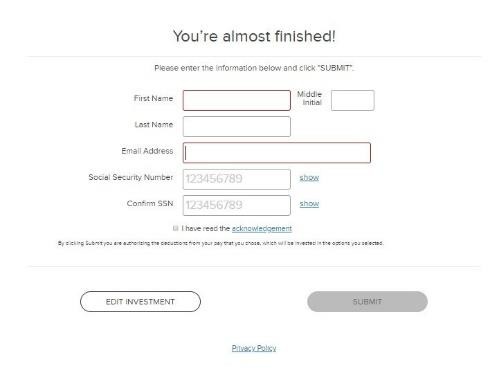

Step 8: Provide personal information

ADP will need your name and Social Security Number so we can identify your account record from your employer and correctly setup your retirement account. Once you have confirmed this information is correct, select “Submit” to compete your enrollment process.

Congratulations on taking your first retirement step!

You have just completed a big step towardssaving for your future retirement.

Prefer to setup your account over the phone?

You have access to ADP’s automated voice response system at 800-MyK-Plan (800-695-7526) 24 hours a day, 7 days a week.

If you need additional assistance one of ADP’s participant service team representatives can help. Representatives are available Monday through Friday, 8 am to 9 pm, Eastern time.

1 Generally available 24 hours a day, 7 days a week except for periods of scheduled maintenance. Customer Service Representatives are registered representatives of ADP Broker-Dealer, Inc. (Member FINRA), an affiliate of ADP, Inc. One ADP Blvd, Roseland, NJ.

ADP, Inc. owns and operates the ADP participant websites and the ADP Mobile Solutions App. ADP, Inc. is a retirement plan record keeper and is not associated with your employer. By delivering this material, ADP, Inc., its affiliates and their employees (“ADP”) are merely providing aneducational service toyour company inaccordance with the terms of ADP’scontract with your employer. ADP Retirement Services is not making any representations about or promoting the services of any third party, nor making any representations about or assuming any responsibility fortheaccuracyand/orcontent ofthese materials, except totheextentsuch materials specifically address or mention ADP and/or its services. Online retirement account access, VRS and Participant Service Team are servicesoffered by ADP Retirement Services.

Descriptions of plan features and benefits are subject to the plan document. The plan document will govern in the event of any inconsistencies. Only licensed representatives of ADP Broker-Dealer, Inc. (ADP BD), Member FINRA, an affiliate of ADP, Inc.

One ADP Blvd, Roseland, NJ 07068 may offer and sell ADP retirement products and services or speak to retirement plan features and/or investment options available in any ADP retirement products. Registered representatives of ADP BD do not offer investment, tax or legal advice to individuals. Please consult with your own advisors for such advice. ADP, the ADP logo and Always Designing for People are registered trademarks of ADP, Inc. All other marks are the property of their respective owners. 99-3884-P-0521 ADPRS-20200928-1379 Printed in USA Copyright © 2015- 2020 ADP, Inc. All Rights Reserved.

BTCM Staffing 401(K) Plan

What kind of Plan is this?

BTCM Staffing 401(k) Plan (“Plan”) has been adopted to provide you with the opportunity to save for retirement on a tax-advantaged basis. This Plan is a type of qualified retirement plan commonly referred to as a 401(k) Plan.

What information does this Summary provide?

This Summary Plan Description (“SPD”) contains information regarding when you may become eligible to participate in the Plan, your Plan benefits, your distribution options, and many other features of the Plan. You should take the time to read this SPD to get a better understanding of your rights and obligations under the Plan.

This Summary addresses the most common questions most Participants may have regarding the Plan. If this SPD does not answer all of your questions, please contact the Administrator or other Plan representative. The Administrator is responsible for responding to questions and making determinations related to the administration, interpretation, and application of the Plan. The name and address of the Administrator can be found at the end of this SPD in the Article entitled “General Information About the Plan.”

This SPD describes the Plan’s benefits and obligations as contained in the legal Plan document, which governs the operation of the Plan. The Plan document is written in much more technical and precise language, and is designed to comply with applicable legal requirements. If the non-technical language in this SPD and the technical, legal language of the Plan document conflict, the Plan document always governs. Likewise, any oral information provided to you regarding the terms of the Plan is not binding on the Plan or the Administrator to the extent it conflicts with the language of the Plan document. If you wish to receive a copy of the legal Plan document, please contact the Administrator.

The Plan and your rights under the Plan are subject to federal laws, including the Employee Retirement Income Security Act of 1974 (ERISA) and the Internal Revenue Code of 1986. Some state laws might indirectly relate to the Plan’s administration. The provisions of the Plan are subject to revision due to a change in laws or due to pronouncements by the Internal Revenue Service (IRS) or Department of Labor (DOL). Your Employer may also amend or terminate this Plan. Your Employer will notify you if the provisions of the Plan that are described in this SPD change.

Types of contributions

- Employee salary deferrals including Roth 401(k) deferrals

- Employer matching contributions

Eligibility Criteria (401K Plan Eligibility Date)

- Age: No Age

- Service: Immediate

- Entry: Date Requirements are met

- Memo Code KH (New) / Accumulator K1 (New): Actual hours are used for vesting purposes.

- Pretax % – Deduction Code 401 (New) / Factor 81 (New)

- Pretax $ – Deduction Code K (New)

- Match – Memo Code KM (New) / Accumulator K3 (New):

- Fixed, each pay period

- Formula is 50% of the first 4% of deferrals

- Catchup contributions are matched

- Non-Elective Contribution (Profit Sharing) – N/A

- 401(k) Loan(S): Your plan allows no loans.

Participation in the Plan

How do I participate in the Plan?

You may become a “Participant” in the Plan once you have satisfied the eligibility requirements and reached your “Entry Date.” The following describes the eligibility requirements and Entry Dates that apply. You should contact the Administrator if you have questions about the timing of your Plan participation.

All Contributions

Excluded Employees: There are no Excluded Employees for purposes of participation in the Plan.

Eligibility conditions: You will be eligible to participate in the Plan on your date of hire. However, you will actually become a Participant in the Plan once you reach the Entry Date as described below.

Entry Date: Your Entry Date will be the date on which you satisfy the eligibility requirements.

What happens if I'm a Participant, terminate employment and then I'm rehired?

If you are no longer a Participant because you terminated employment, and you are rehired, then you will be able to participate in the Plan on your date of rehire provided you are otherwise eligible to participate in the Plan.

Employee Contributions

What are salary deferrals and how do I contribute them to the Plan?

Annual Dollar Limit: You should also be aware that each separately stated annual dollar limit on the amount you may defer (the annual deferral limit and the “catch-up contribution” limit) is a separate aggregate limit that applies to all such similar salary deferral amounts and “catch-up contributions” you may make under this Plan and any other cash or deferred arrangements (including tax-sheltered 403(b) annuity contracts, simplified employee pensions or other 401(k) plans) in which you may be participating. Generally, if an annual dollar limit is exceeded, then the excess must be returned to you in order to avoid adverse tax consequences. For this reason, it is desirable to request in writing that any such excess salary deferral amounts and “catch-up contributions” be returned to you.

If you are in more than one plan, you must decide which plan or arrangement you would like to return the excess. If you decide that the excess should be distributed from this Plan, you must communicate this in writing to the Administrator not later than the March 1st following the close of the calendar year in which such excess deferrals were made. However, if the entire dollar limit is exceeded in this Plan or any other plan your Employer maintains, then you will be deemed to have notified the Administrator of the excess. The Administrator will then return the excess deferrals and any earnings to you by April 15th.

Employee Contributions

In addition to any deferrals, you elect to make, your Employer will make additional contributions to the Plan. This Article describesEmployer contributions that will be made to the Plan and how your share of the contribution is determined.

What is the Employer matching contribution and how is it allocated?

What are forfeitures and how are they allocated?

Distributions Prior to Termination and Hardship Distributions

In-Service Distributions: You may be entitled to receive an in-service distribution. However, this distribution is not in addition to your other benefits and will therefore reduce the value of the benefits you will receive at retirement. This distribution is made at your election and will be made in accordance with the forms of distributions available under the Plan.

Conditions and Limitations: Generally you may receive a distribution from the Plan from certain accounts prior to your termination of employment provided you satisfy the condition described below:

You have attained age 59 1/2

The following limitations apply to in-service distributions from certain accounts:

The minimum amount you can receive as an in-service distribution is $500.

You may elect to limit the source of an in-service withdrawal to your Roth Elective Deferral Account, rollovers of Roth Elective Deferrals held in your Rollover Account.

Qualified Reservist Distributions: If you were/are:

(i) A reservist or national guardsman.

(ii) Called to active duty after September 11, 2001.

(iii) Called to duty for at least 180 days or for an indefinite period, you may take a distribution of your elective deferrals under the Plan while you are on active duty, regardless of your age. The 10% premature distribution penalty tax, normally applicable to Plan distributions made before you reach age 59 1/2, will not apply to the distribution. You also may repay the distribution to an IRA, without limiting amounts you otherwise could contribute to the IRA, provided you make the repayment within 2 years following your completion of active duty.

Can I withdraw money from my account in the event of financial hardship?

Hardship Distributions: You may withdraw money for financial hardship if you satisfy certain conditions. This hardship distribution is not in addition to your other benefits and will therefore reduce the value of the benefits you will receive at retirement.

Qualifying Expenses: A hardship distribution may be made to satisfy certain immediate and heavy financial needs that you have. A hardship distribution may only be made for payment of the following:

(a) Expenses for medical care (described in Section 213(d) of the Internal Revenue Code) previously incurred by you, your spouse, your dependents or your beneficiaries or necessary for you, your spouse, your dependents or your beneficiaries to obtain medical care.

(b) Costs directly related to the purchase of your principal residence (excluding mortgage payments).

(c) Tuition, related educational fees, and room and board expenses for the next twelve (12) months of post-secondary education for yourself, your spouse, your dependents or your beneficiaries.

(d) Amounts necessary to prevent your eviction from your principal residence or foreclosure on the mortgage of your principal residence.

(e) Payments for burial or funeral expenses for your deceased parent, spouse, children, other dependents or beneficiaries.

(f) Expenses for the repair of damage to your principal residence that would qualify for the casualty deduction under the Internal Revenue Code.

To determine whether a Participant is entitled to a hardship distribution, a beneficiary is someone you designate under the Plan to receive your death benefit who is not your spouse or dependent.

Conditions: If you have any of the above expenses, a hardship distribution can only be made if you certify and agree that all of the following conditions are satisfied:

(a) The distribution is not in excess of the amount of your immediate and heavy financial need. The amount of your immediate and heavy financial need may include any amounts necessary to pay any federal, state, or local income taxes or penalties reasonably anticipated to result from the distribution.

(b) You have obtained all distributions, other than hardship distributions, and all nontaxable loans currently available under all plans that your Employer maintains.

(c) If the hardship distribution is made from the Participant’s Elective Deferral Account, that you will not make any salary deferrals for at least six (6) months after your receipt of the hardship distribution. If your salary deferrals are suspended, then your deferral election that was in place prior to the suspension will continue in effect after the suspension.

Limitations: The following limitations apply to hardship distributions:

The minimum amount you can request as a hardship distribution is $500.

You must be employed with the Employer at the time of the hardship distribution.

Account Restrictions: There are restrictions placed on hardship distributions which are made from certain accounts. These accounts are the ones set up to receive your salary deferral contributions and other Employer contributions which are used to satisfy special rules that apply to 401(k) plans. Generally, the only amounts that can be distributed to you on account of a hardship from these accounts are your salary deferrals. The earnings on your salary deferrals and special Employer contributions may not be distributed to you on account of a hardship. Ask the Administrator if you need further details.

Benefits and Distributions Upon Termination of Employment

When can I get money out of the Plan?

You may receive a distribution of the vested portion of some or all of your accounts in the Plan for the following reasons:

Death

Normal retirement

Disability

Termination of employment for reasons other than death, disability or retirement

This Plan is designed to provide you with retirement benefits. However, distributions are permitted if you die or become disabled. In addition, certain payments are permitted when you terminate employment for any other reason. The rules under which you can receive a distribution are described in this Article. The rules regarding the payment of death benefits to your beneficiary are described in “Benefits and Distributions Upon Death.”

You may also receive distributions while you are still employed with the Employer. (See the Article entitled “Distributions Prior to Termination and Hardship Distributions” for a further explanation.)

Military Service: If you are a veteran and are reemployed under the Uniformed Services Employment and Reemployment Rights Act of 1994, your qualified military service may be considered service with the Employer. There may also be benefits for employees who die or become disabled while on active duty. Employees who receive wage continuation payments while in the military may benefit from various changes in the law. If you think you may be affected by these rules, ask the Administrator for further details.

Distributions for Deemed Severance of Employment: If you are on active duty for more than 30 days, then the Plan generally treats you as having severed employment for distribution purposes. This means that you may request a distribution from the Plan. If you request a distribution on account of this deemed severance of employment, then you are not permitted to make any contributions to the Plan for six (6) months after the date of the distribution.

What happens if I terminate employment before death, disability or retirement?

If your employment terminates for reasons other than death, disability or normal retirement, you will be entitled to receive only the “vested percentage” of your account balance.

You may elect to have your vested account balance distributed to you as soon as administratively feasible following your termination of employment. However, if the value of your vested account balance does not exceed $5,000, then a distribution will be made to you regardless of whether you consent to receive it. (See the question entitled “How will my benefits be paid to me?” for additional information.)

What happens if I terminate employment at Normal Retirement Date?

Normal Retirement Date: You will attain your Normal Retirement Age when you reach age 65. Your Normal Retirement Date is the date on which you attain your Normal Retirement Age.

Payment of Benefits: You will become 100% vested in all of your accounts under the Plan once you attain your Normal Retirement Age. However, the actual payment of benefits generally will not begin until you have terminated employment and reached your Normal Retirement Date. In such event, a distribution will be made, at your election, as soon as administratively feasible. If you remain employed past your Normal Retirement Date, you may generally defer the receipt of benefits until you actually terminate employment. In such event, benefit payments will begin as soon as feasible at your request, but generally not later than age 70 1/2. (See the question entitled “How will my benefits be paid to me?” for an explanation of how these benefits will be paid.)

What happens if I terminate employment due to disability?

Definition of Disability: Under the Plan, disability is defined as a physical or mental condition resulting from bodily injury, disease, or mental disorder which renders you incapable of continuing any gainful occupation and which has lasted or can be expected to last for a continuous period of at least twelve (12) months. Your disability must be determined by a licensed physician. However, if your condition constitutes total disability under the federal Social Security Act, then the Administrator may deem that you are disabled for purposes of the Plan.

Payment of Benefits: If you become disabled while an employee, you will be entitled to your vested account balance under the Plan. Payment of your disability benefits will be made to you as if you had retired. However, if the value of your vested account balance does not exceed $5,000, then a distribution of your vested account balance will be made to you, regardless of whether you consent to receive it. (See the question entitled “How will my benefits be paid to me?” for an explanation of how these benefits will be paid.)

How will my benefits be paid to me?

Forms of Distribution: If your vested account balance does not exceed $5,000, then your vested account balance may only be distributed to you in a single lump-sum payment.

In addition, if your vested account balance exceeds $5,000, you must consent to any distribution before it may be made. If your vested account balance exceeds $5,000, you may elect to receive a distribution of your vested account balance in:

(a) A single lump-sum payment

(b) Installments over a period of not more than your assumed life expectancy (or the assumed life expectancies of you and your beneficiary)

(c) Partial withdrawals. You may elect to limit the source of such a partial withdrawal to amounts attributable to (1) your Rollover Account, including amounts attributable to rollovers of Roth Elective Deferrals (2) your Roth Elective Deferral Account, rollovers of Roth Elective Deferrals held in the Rollover Account.

Delaying Distributions: You may delay the distribution of your vested account balance unless a distribution is required to be made, as explained earlier, because your vested account balance does not exceed $5,000. However, if you elect to delay the distribution of your vested account balance, there are rules that require that certain minimum distributions be made from the Plan. If you are a 5% owner, distributions are required to begin not later than the April 1st following the end of the year in which you reach age 70 1/2. If you are not a 5% owner, distributions are required to begin not later than the April 1st following the later of the end of the year in which you reach age 70 1/2 or retire. You should contact the Administrator if you think you may be affected by these rules.